Food delivery giant Swiggy finds itself at a critical juncture, and it’s almost a make-or-break time for its big bet on quick commerce.

Despite getting a thumbs-up from brokerages for the potential upside in the long run, a surge in losses for Q4 FY2025, primarily fueled by its aggressive expansion of Instamart is a worrying sign.

Undoubtedly, the revenue growth is a positive factor for Swiggy, but the fact is that it has fallen deeper into the red. Over the past year, we have seen the Instamart and quick commerce boom, the launch of new services and verticals, and the much-heralded Swiggy IPO, but profits have eluded the Sriharsha Majety-led company.

The stock market’s reaction has been telling. Despite a brief intra-day rally post-results, Swiggy’s stock recently touched an all-time low of INR 297 in the middle of last week, before recovering slightly to INR 321.15, which is still more than 20% below its listing price of INR 420.

This raises a pressing question: can Swiggy navigate this cash-intensive growth phase and emerge profitable, or is it digging a hole too deep to escape?

The Instamart HoleSwiggy’s Q4 FY25 results painted a stark picture of its current situation. The company’s consolidated net loss nearly doubled year-on-year, ballooning to a staggering INR 1,081.18 Cr. This was 35% higher than the INR 799 Cr loss in Q3 FY25.

Revenue from operations showed some spark, rising sharply by 44.8% year-on-year to INR 4,410 Cr in Q4 FY25. On an EBITDA level, significant growth investments in quick commerce took a toll, and Instamart itself incurred an operational loss of INR 770.9 Cr in the quarter.

This was driven by an unprecedented expansion, where Swiggy added 316 new dark stores – more than the previous eight quarters put together – and deploying INR 425 Cr in capex in Q4 alone. This aggressive push, coupled with increased customer incentives, led to underutilised network capacity and elevated burn.

Operating revenue for Instamart soared as a result of these investments, more than doubling YoY to INR 689.1 Cr and a similar growth was seen in the gross order value (GOV) and monthly transacting users.

Swiggy CEO Majety acknowledged the “rapid expansion phase” and “high competitive intensity,” but stated that Instamart likely reached its “peak of adjusted EBITDA losses” in late Q4 and things are only going to improve. But that’s not what the competition is saying.

Eternal-owned Blinkit’s adjusted EBITDA loss widened over 381% to INR 178 Cr in the March quarter. While this is not as severe as Swiggy, even Eternal acknowledged that the next few quarters will continue to see a ramp up in investments and profitability will therefore be impacted.

It’s hard to see where the profitability turning point will come for either company after years of saying that quick commerce was on the verge of profits.

Food Delivery Remains A RockIn contrast to the tumultuous quick commerce segment, both companies are relying on profitability in the food delivery space to fund the expansion.

Swiggy’s core food delivery business was stable with a PAT of INR 220.5 Cr, a more than four-fold increase YoY. Surprisingly, Swiggy Bolt — the 10-minute delivery service launched last year — accounted for 12% of food delivery orders, and its new app Snacc is said to be showing early promise.

Eternal’s Zomato notably shut down Zomato Quick, which was its competition to Bolt, citing poor customer experience and limited incremental demand. This divergence in strategy for rapid food delivery indicates a forking in the market and shows that Swiggy has a greater risk appetite at the moment.

Overall though, both former food delivery rivals seem to diverge on the quick commerce front largely, and primarily on execution.

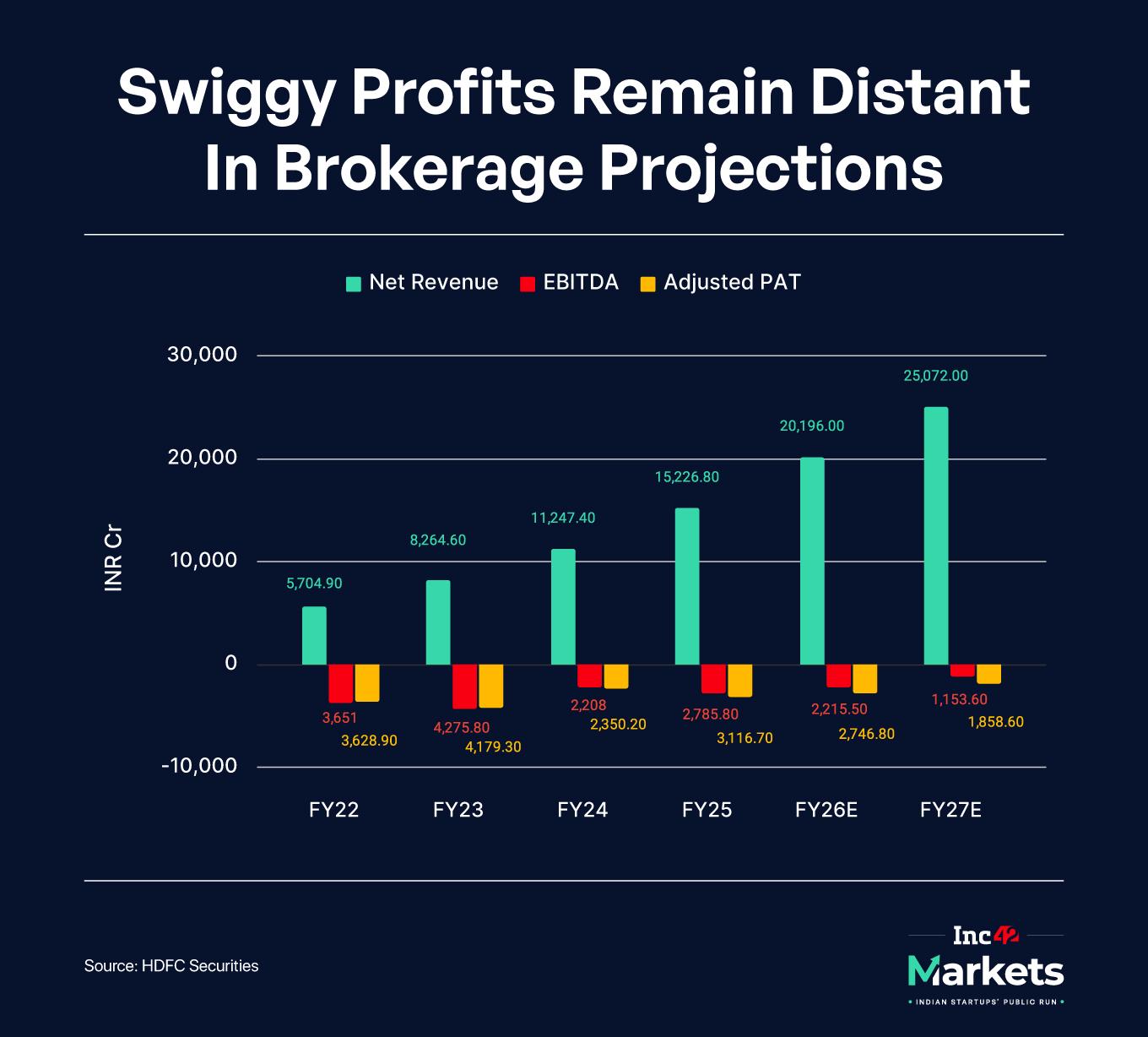

Despite the higher losses, HDFC Securities has upgraded Swiggy to ‘Buy’ (from ‘Reduce’), signalling a belief in the company’s long-term potential. Like HDFC Securities, brokerage Anand Rathi also believes that Swiggy remains undervalued due to the market not yet factoring in quick commerce completely.

Anand Rathi acknowledged the execution gap in quick commerce compared to Eternal-owned Blinkit, but pointed to Swiggy’s stock correction of nearly 50% over the past five months, which has created a more attractive valuation.

Swiggy’s Big ChallengeHDFC Securities stated, “At the current market price, we are effectively valuing the Instamart business at only INR 7,500 Cr (less than $1 Bn), offering a compelling value with a two-year cash burn runway.”

Swiggy’s path forward is fraught with a great many challenges, it’s certainly not going to be easy to wrestle with quick commerce’s many moving parts and extract profits.

While brokerages have shown some bullishness this past week, this rests on the premise that the current heavy investment in Instamart will build a dominant market position. At the moment, Swiggy is trailing Zomato on revenue scale and at the end of FY24, it was behind Zepto as well. We don’t know whether Swiggy will occupy the third position at the end of FY25, but if it does, the increased investment in quick commerce might be questioned.

The competitive intensity is such that there’s no guarantee that this investment will unlock the position. While operational efficiencies will eventually kick in, turning the segment profitable will take a combination of new scale and profitable growth in existing markets.

Blinkit and Zepto are vying for market share, and the period of high cash burn will continue for the time being. If Swiggy fails to close the execution gap with Blinkit, or if its average order values and take-rates don’t improve as projected, the path to profitability for Instamart could be significantly delayed.

There’s also a question of whether Swiggy is going a bit too slow on Instamart when the rest of the competition seems to be doubling down on increasing density within cities. Swiggy Instamart has just over 1,000 dark stores, as compared to Blinkit’s 1,500+ count, but in terms of revenue, there’s a huge chasm between the two platforms.

Brokerages believe losses in quick commerce may gradually unwind as operations are optimised, take rates improve, and AOVs rise. HDFC Securities, for instance, does not expect Swiggy to have positive EBITDA till FY27.

There are some concerns about investor fatigue if losses continue to mount without a clear and convincing turnaround story, especially relevant for a company yet to go public.

For CEO Majety and the Swiggy inner circle, the next three to five quarters will be critical. The market will be keenly watching bottom lines and how the company’s expansion is coming along. Analysts expect Swiggy to increase the customer monetisation touchpoints within Instamart. One could see platform fees being increased to make up for the higher investment.

It worked to bring food delivery towards profits, will the same formula work for quick commerce and Swiggy Instamart?

Stocks In Focus: India-Pak Conflict Creates Travel HeadachesIt’s been a torrid two weeks for travel tech companies as consumers were forced to cancel flight bookings and change plans in light of travel and airspace restrictions due to the cross-border clashes between India and Pakistan.

And swept up in nationalistic fervour, many travel tech platforms also announced a boycott for bookings to Turkey and Azerbaijan, seen as Pakistan’s allies in the fight, .

And to round off this eventful week, there was a controversy as EaseMyTrip’s Nishant Pitti accused MakeMyTrip of leaking data about defence personnel to Chinese investors. That resulted .

Indeed, travel was a strong theme even in terms of the Q4 disclosures, as MakeMyTrip and ixigo both released their financials too. While ixigo’s 127% to INR 16.8 Cr in Q4 FY25 from INR 7.4 Cr, MakeMyTrip saw its .

When it came to the stock market, EaseMyTrip had the worst time among them all, falling by close to 5% even as most other listed new-age tech companies showed some gain.

- Bengaluru-based cloud kitchen startup Curefoods has converted into a public company as it ramps up preparations for its initial public offering

- The fair value of SoftBank Vision Fund II’s public portfolio companies dwindled 21.7% sequentially in Q4 FY24 due to fall in share prices of Swiggy and Ola Electric, both listed companies

- The Policybazaar parent’s PAT zoomed 2.8X to INR 170.7 Cr in Q4 FY25 with revenue crossing the INR 1,500 Cr mark in the quarter

- Investment tech startup Groww is planning to file draft papers with market regulator for an IPO through a confidential pre-filing route in the next two weeks

- The logistics giant reported another profitable quarter with net profits of INR 72.6 Cr in Q4 FY25 as against a loss of INR 68.5 Cr in the year-ago quarter

The post appeared first on .

You may also like

Romanians to vote between nationalist Simon and pro-EU Dan in tight presidential election rerun

International Museum Day Today: Shooting Stars, Vintage Lamps, Impact Diamonds & Delhi Sultanate Weights

Neeraj Chopra Makes History with 90m Javelin Throw: Odisha Leaders Celebrate

Trump to speak with Putin, Zelensky on Monday

Uttar Pradesh: 2 Animals At Kanpur Zoo Test Positive For Bird Flu; Disinfection Carried Out